Lenders is not only their HOA charges plus borrowing cards, car loans, and home loan on your own month-to-month property expenditures, which means it apply at your own DTI ratio.

A higher DTI ratio mode you might be thought to be a more Magnolia savings and installment loan impressive exposure because the more of your earnings is already spoken to have. So, if the HOA charges are high, your DTI ratio increases, which could make they more challenging so you can qualify for home financing.

Look at it given that an equilibrium level – on one side, you may have your revenue, as well as on one other, the money you owe. The trick is to contain the size balanced, or even better, angled and only earnings.

Example Situations

- Scenario 1: Think you may be to shop for a flat with an HOA payment from $300 monthly. The monthly earnings are $5,000, and also you have $step one,000 in other debts (for example car costs and you may student education loans).When you are the $three hundred HOA payment, your own full monthly debt obligations diving so you’re able to $1,3 hundred. It means their DTI ratio became twenty-six%.Should your lender’s restrict appropriate DTI ratio are 25%, this seemingly brief HOA commission may be the really topic one stands anywhere between your mortgage acceptance.It’s sometime such as for example being ready to board a journey simply to get averted because your handbag is but one lb more than the extra weight limitation. Frustrating, correct?

- Circumstances 2: Picture this: you are torn between a couple of houses you positively like. One has good $150 month-to-month HOA commission, in addition to other enjoys nothing. Without the payment, you could qualify for a $three hundred,000 home loan.Although not, with the percentage, the financial institution might only approve your to possess $270,000. Its an understated huge difference but a vital one. One $31,000 you’ll mean the essential difference between providing a home with all the advantages you prefer or being required to give up.

Conclusions

Navigating the industry of homeownership is somewhat problematic, particularly when considering figuring out in the event the HOA fees try element of their mortgage. However now you to we eliminated the new fog to it, it must be a breeze.

We dove to the nitty-gritty out-of if HOA costs are part of your home loan repayments, the way they apply at your overall construction will set you back, and you will all you have to keep in mind when cost management for a property inside an enthusiastic HOA neighborhood.

TL;DR? Is HOA charge as part of the financial? No, they are not; HOA charges are often separate out of your financial.

However, if you find yourself HOA fees may possibly not be element of the mortgage, they’re nonetheless an option little bit of the fresh puzzle with regards to into the overall houses costs. Overlooking them you’ll toss a great wrench on the monetary arrangements, therefore it is vital to grounds them for the regarding the score-wade.

Secret Takeaways

- Constantly are HOA costs on your own month-to-month funds to end unexpected situations.

- Consult your lender to learn how HOA costs you’ll perception your loan approval.

- Manage your profit smartly to be sure HOA costs dont threaten your mortgage.

Need help learning HOA fees and your home loan? Get support from your professional HOA attorneys to ensure you are making an informed financial conclusion for the coming. Be an associate now, and let’s provide focused!

The word may appear a little while perplexing, very let’s clear up exactly what a keen HOA home loan is actually. Your mortgage is the loan you are taking over to get your household. Think of it due to the fact vehicles you’ve chosen because of it travels (the house-to order procedure).

Instead, and also make lifetime also much easier, automated costs will be arranged, ensuring you don’t skip a deadline. Of a lot HOAs promote electronic repayments, the spot where the costs is deducted from the family savings as opposed to you having to elevator a thumb.

New Part regarding Escrow Profile

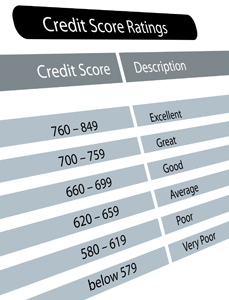

To find this out, it calculate one thing called the financial obligation-to-earnings (DTI) ratio. That it proportion is simply a measure of how much cash of money would go to paying off expenses.